Estimated reading time: 5 minutes

Full report on Scotland’s Flex landscape by Steven Carr can be found here

5 Key Insights Shaping Scotland’s Flexible Workspace Landscape in 2026

Key Takeaways

- Scotland now has 391 flexible workspace locations, a 40% increase from previous estimates.

- Glasgow and Edinburgh lead the market, but regional clusters are growing rapidly in areas like West Scotland and East Scotland.

- Independent operators and non-profits make up nearly 70% of the market, promoting a community-driven approach.

- Traditional business centers still dominate, while hybrid models and micro-spaces are on the rise.

- The flexible workspace landscape in Scotland is larger, more diverse, and positioned for sustained growth over the next few years.

Research in March 2026 by Your Flex Expert Ltd shows there are around 391 flexible workspaces’ (Coworking, Business Centres, Serviced Offices, Flex Industrial and flexible studios) in Scotland. 37% of these are traditional business centres, and 30% are coworking spaces.

Scotland’s flexible workspace sector is undergoing one of its most significant periods of growth and transformation in over a decade.

With 391 flexible workspace locations, 199 operators, and a rapidly diversifying mix of serviced offices, coworking hubs, incubators, and flex‑industrial spaces, the market is far larger and more dynamic than previously reported.

Below, we break down five major insights that reveal where the market is heading — and what it means for operators, landlords, and businesses choosing where to work.

1. Scotland’s Flexible Workspace Market Is Much Larger Than Previously Reported

For years, Scotland’s flexible workspace footprint was underestimated. Earlier press coverage cited 279 locations, but updated research shows the true figure is 391 — a 40% larger market than previously understood. yourflexexpert.co.uk

Why this matters

- Investors and landlords have been operating with incomplete data.

- The sector’s economic contribution — including 600+ jobs — is significantly higher than assumed.

- Growth is not limited to major cities; regional and rural hubs are expanding too.

This expanded dataset positions Scotland as one of the UK’s most diverse and community‑driven flexible workspace ecosystems.

2. Glasgow and Edinburgh Dominate — But Regional Clusters Are Rising Fast

The “big four” cities — Glasgow, Edinburgh, Aberdeen, and Dundee — account for 48% of all Scottish flexible workspaces. Glasgow leads with 77 locations, closely followed by Edinburgh with 71.

Regional highlights

- West Scotland is the largest region (34.8%), driven by Glasgow’s density of business centres and coworking hubs.

- East Scotland (23.2%) is powered by Edinburgh’s mix of serviced offices and boutique coworking spaces.

- Tayside & Fife (13.6%) is emerging as a strong third cluster, with a healthy mix of independents and incubators.

- Highlands & Islands (6.1%) shows meaningful growth in micro‑spaces and community hubs.

What this means for 2026

Demand is no longer concentrated in city centres. Suburban and rural operators — especially community‑led hubs — are becoming essential infrastructure for local economies.

3. Independent Operators and Non‑Profits Are the Backbone of the Market

One of the most striking insights is the dominance of small, local operators:

- Independent operators (1 location): 29.2%

- Incubators & non‑profits: 22%

- Small chains (2–4 locations): 18.7%

yourflexexpert.co.uk

This means nearly 70% of Scotland’s flexible workspace market is locally rooted, community‑driven, and often mission‑led.

Why this matters

- Scotland’s market is less corporate and more community‑focused than other UK regions.

- Non‑profits and CICs play a major role in supporting underserved groups, creatives, and rural communities.

- Collaboration networks like Connected Hubs Scotland strengthen regional resilience and knowledge‑sharing.

In contrast, global players like IWG account for just 9.2% of the market — though IWG remains the single largest operator with 36 Scottish locations. yourflexexpert.co.uk

4. Traditional Business Centres Still Lead — But Hybrid Models Are Growing

Despite the rise of coworking culture, traditional serviced business centres remain the largest workspace type in Scotland:

| Workspace Type | % of Market |

|---|---|

| Traditional Business Centres | 36.6% |

| Coworking Spaces | 30.2% |

| Full‑Service Flex | 23.5% |

| Creator/Maker Spaces | 6.9% |

| Managed Offices | 4.1% |

| Mixed‑Use Flex | 3.8% |

Key takeaways

- Traditional serviced offices still dominate because SMEs value privacy, stability, and predictable costs.

- Coworking continues to grow, especially in boutique and micro‑spaces.

- Full‑service flex (meeting rooms, coworking, private offices, amenities) is expanding fastest in major cities.

- Creator and maker spaces — though niche — are vital for Scotland’s creative economy.

This mix shows a market that is both mature and diversifying, with room for innovation across all segments.

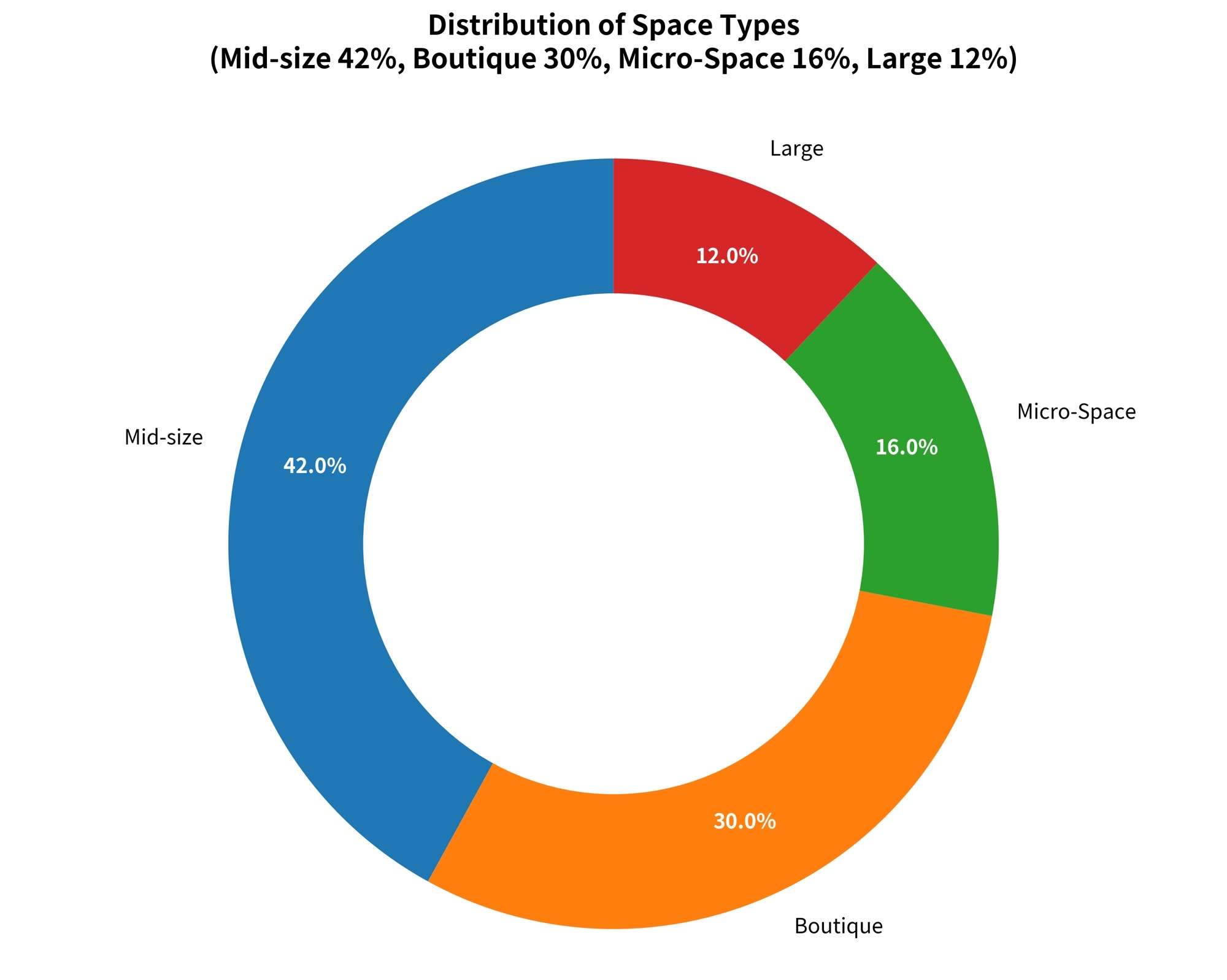

5. Mid‑Sized Workspaces Are the Market’s Core — But Micro‑Spaces Are Rising

When analysing workspace size, one category stands out:

- Mid‑sized spaces (7,000–20,000 sq ft): 41.9%

- Boutique spaces (1,000–7,000 sq ft): 30.2%

- Micro‑spaces (<1,000 sq ft): 16.1%

- Large spaces (>20,000 sq ft): 11.8%

What this tells us

- Mid‑sized business centres remain the backbone of Scotland’s flex market.

- Boutique spaces reflect the strength of independent operators and community‑led hubs.

- Micro‑spaces are increasingly important in rural towns, islands, and regeneration areas.

- Large corporate flex centres remain rare — consistent with Scotland’s SME‑heavy economy.

Staffing insight

Across all workspace types, the average staffing level is 1.5 FTE per location, highlighting how lean and efficient most operators are. yourflexexpert.co.uk

Conclusion: A Bigger, More Diverse, More Community‑Driven Market Than Ever

Scotland’s flexible workspace landscape in 2026 is:

- Larger than any previous report suggested

- More diverse, spanning everything from micro‑coworking hubs to full‑service flex centres

- More community‑driven, with independents and non‑profits shaping the sector

- Growing fast, fuelled by hybrid work, SME expansion, and corporate downsizing

With strong demand in both major cities and regional markets — and operators signalling plans for further expansion — Scotland is positioned for sustained growth in flexible workspace over the next 3–5 years.